Debunking Economists (Plus Deep Dive on Google)

Debunking Economists (Plus Deep Dive on Google)

Why people still call for recession

Welcome to the free midweek edition of MktContext. I am a professional money manager who runs a $5B fund and loves writing about the market. We’ll help you improve your investment returns by understanding the economy and timing the stock market. Subscribe for free weekly insights:

We’ve been able to capture all of the upside in this roaring bull market, while avoiding the pitfalls. Check out our past archive to see market timing in action!

False checklists

I am continually amazed by the number of smart people calling for an imminent recession. Economists at every major bank have a “checklist” they use with multiple indicators to gauge a recession. Many have been sounding the recession alarm for a long time now. Let’s dive deeper into each indicator.

The first one that comes up is the yield curve. The argument goes, every yield curve inversion (i.e. long-term interest rates are below short-term rates) has led to recession. But as we wrote, the economy is less sensitive to interest rates nowadays, and the Fed/Treasury are artificially suppressing the curve. So the signal has been a dud in this cycle.

Next up is unemployment. We’ve written ad nauseum on the labor market. Our view is the official unemployment statistics are being fooled by immigration and reclassifications. Plus, there is ongoing normalization post labor shortages:

The third common indicator is the Conference Board “Leading Economic Indicators”. This is itself a basket of indicators that supposedly predict economic weakness. According to the Board, the first driver of LEI weakness is yield curve inversion, which we already discussed. The second is based on manufacturing, which makes up a negligible part of the economy. The third is based on consumer sentiment which has been notoriously incongruent with actual spending patterns.

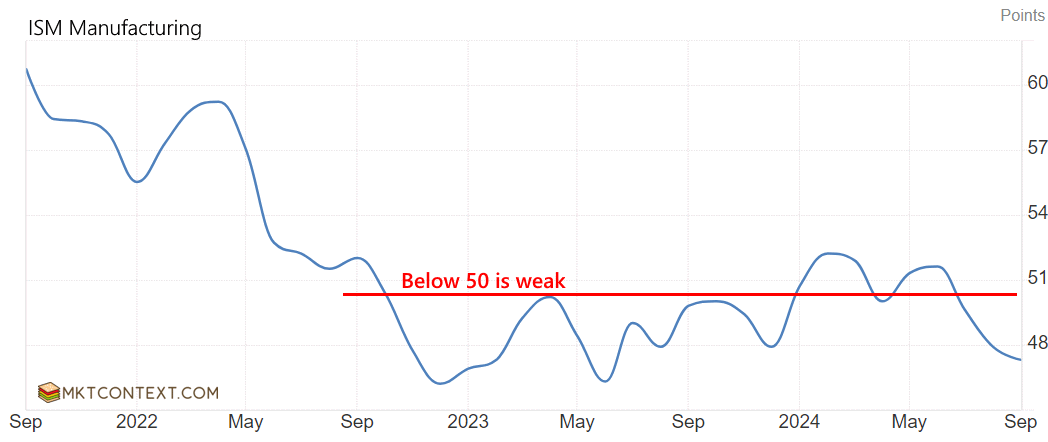

The fourth indicator is manufacturing. People went on an online shopping spree during Covid lockdowns and are no longer interested in buying material things. Instead they are spending it on services like restaurants and vacations. So the manufacturing sector has been depressed for many quarters now (chart below), but that is not reflective of consumer spending patterns.

And the last indicator, Fed interest rate vs GDP, which tells us the Fed is slamming on the brakes of the economy. But we know raising interest rates hasn’t been effective in quelling activity. Consumers and businesses have reduced debt and locked in low rates, which means they’re less impacted by higher interest. Furthermore, people have ample cash saved up from roaring stock markets and Covid-era government stimulus.

Add all this up, and it’s clear the checklist is not recessionary at all. But economists are stuck using outdated models (“they always worked before!”) in an unprecedented cycle. This is why we study the economy closely to understand what’s really going on.

There is a large cohort of investors out there who genuinely believe a recession is coming. In contrast, we believe the bull rally is fundamentally justified and would not be on the sidelines with cash.

Share this post with someone who wants to earn money in the stock market!

ASML Earnings Miss

The big news on Tuesday was ASML’s massive miss and earnings revision down. ASML is a semiconductor capital equipment maker or “semicap”, supplying machinery to TSMC which makes chips for NVDA. If NVDA makes the picks and shovels for AI, then TSMC stamps the metal and ASML makes the forging equipment.

ASML makes a unique type of lithography tool that no one else in the world can make. So when their earnings decelerate, the whole world watches. There appears to be two issues: 1) their key customers are slowing upgrades, and 2) China is nearing the end of a massive capex spree.

The CFO tried to assure investors that AI momentum continues, but it’s the other segments that are weak. Regardless, this will have ramifications across the entire mega-cap tech ecosystem. NVDA and the other AI stocks are down in sympathy today. At the same time, there were announcements of more export restrictions on NVDA.

We’ll have more to say on this topic as we hear from other companies. Suffice to say, the October-end volatility we predicted is already rearing its ugly head.

From time to time I’ll share articles from incredible finance authors. This excerpt on Google is timely as tech is bullish and GOOG has lagged its Mag7 peers of late. Written by J. Nicholas, who publishes excellent weekly stock reports. The full post can be found here.

Just Google It

Google is an advertising business. It makes money by leveraging the attention of billions of people using its search engine product to attract advertisers that want to sell products to you. Advertising is Google’s core business—it’s their peanut butter and jelly. If you were to add up all advertising-related revenue of the company and express it as a percentage, that number would be roughly 77% of total sales. Most of this revenue is thanks to Search.

With the dominance of the search business and the massive amount of data Google now has on you from your use of its many services, Google can advertise to you more effectively, thereby making more money off you. Google’s ability to gather so much data from a variety of products and services and sources is what gives Google its world class advertising platform and global market dominance.

AI strategy: Since the launch of ChatGPT, companies have made a big push into LLMs, racing to be the leader in the new technological revolution of artificial intelligence. AI spending at Google has hit somewhere near $14 billion per year as of the time of writing, mostly related to cloud architecture spending (Nvidia chips) and building out data centres. This spending is hurting Google’s free cash flow greatly, which has led investors (me included) to wonder if this spending will actually yield returns.

Unlike OpenAI, which is the current undisputed leader in the AI model and LLM space, Google has much more user data to train these models and has been developing AI for over a decade. Remember those many popular products and services that Google owns and the 2 trillion(+) annual Search queries Google processes every year? With those alone, Google has an almost endless source of data in its current position.

Regulatory scrutiny: In August, the U.S. Department of Justice won a case deeming Google an illegal monopoly. Just last week, Google was hit with a court order to open up its app store to rivals, and we learned that the U.S. Justice Department may soon ask a judge to break up the company. This has scared many investors, causing the stock to drop roughly 22% from its highs in June.

While this seems alarming at first glance, a breakup might actually turn out to be a bonus for you as a shareholder. The many individual companies Google owns will almost surely be valued at a much higher valuation when they’re individually owned rather than wholly owned by Google.

Growth: There are three main markets Google has entered that are projected to grow exponentially and consistently over the next decade…

The above is just an excerpt of the full article. Visit J. Nicholas on Substack to read the rest of this deep dive including fundamentals, price target, and more.

That’s it for today!

If you like our content, click the button below to subscribe. Our free weekly letters will teach you how to use economic data and technical analysis to make money in the market. We’ve been timing the stock market (and beating it) since 2014.

Disclaimer: This publication is for educational purposes only. The authors are not investment advisors and nothing here is investment advice. Always do your own due diligence.