🍔Cracks in the Economy

An economic slowdown is underappreciated by the market

Another Monday, another gap down. Our skew indicator remains prescient as we called for the pullback in SPX. Now that it has run its course, find out what the next move in the market will be. But beware, because cracks are starting to form in the economy.

In this week’s article we discuss the outcome of the tariff war, and offer three timely investment ideas that will help boost your portfolio. So what are you waiting for? Join us in market timing today!

Cracks in the economy

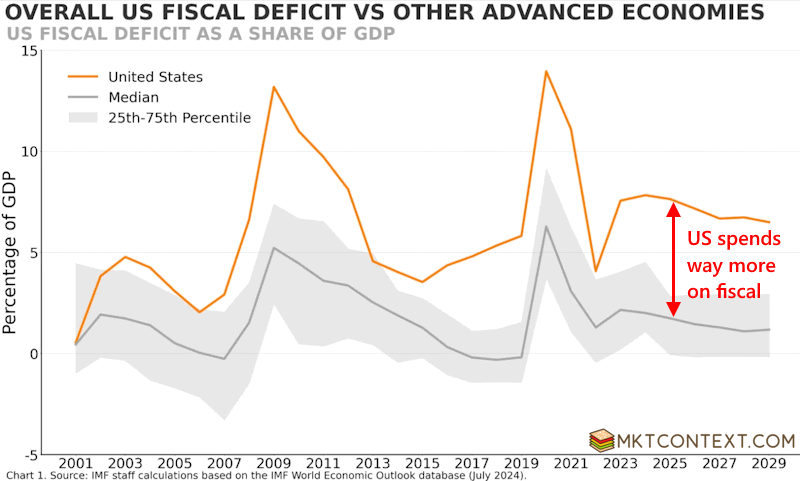

Fiscal spending has been a big part of our bull thesis on US exceptionalism. Since the Covid pandemic, the US has led the world in government spending to support the economy, whereas other countries (notably Europe) were austere. This is a major reason why the US avoided a recession in 2022 and why US equity markets have outperformed everything else.

That might reverse now. With all the cuts to be made by the Department of Government Efficiency (DOGE), it’ll have a negative impact on fiscal spending. Many of the cuts take away from domestic programs that represent real investments and real jobs. In addition, government-funded sectors (healthcare, education, etc) have been propping up the jobs numbers as we wrote back in November. An across-the-board DOGE headcount reduction is not going to bode well for the economy.

For the US exceptionalism story to continue, you need the private sector to pick up the hiring slack. Unfortunately, private job growth has been decelerating and is now only growing 1.3% annually. Trump’s tax incentives will spur private hiring, but won’t take effect until the second half of the year. We wouldn’t be surprised if small biz optimism takes a dive next month, what with all the gnashing about tariffs.

“But aren’t the spending cuts reinvested into the economy in the form of tax cuts? Shouldn’t that offset the fiscal drag?” The answer is twofold. Firstly, the net spend is still decreasing because that’s the only way to reduce the public debt burden. Secondly, it comes down to propensity to spend. Gov’t programs, especially inefficient ones, are guaranteed to spend the money they’re granted. Private businesses do not spend all of their tax cut dollars; some is kept to pad profit margins. Dollar-for-dollar, fiscal spend is being redirected in a way that reduces spending velocity.

So there’s risk to the economic growth story. We called out in January that the US Econ Surprise index is already rolling over (shown below). We got fresh warning this week with weakness in: job postings (JOLTS), unemployment claims, non-farm payrolls, services PMI, and consumer confidence, all surprising to the downside. GDP estimates were taken down from 3.9% to 2.9%. That’s a lot of bad news in one week that was largely ignored by the market. We reiterate that the market is underpricing the risk of a growth scare or unemployment shock.

As proof, the US 10-year rate fell back to 4.4% despite escalating tariff jabs. Bonds are more sensitive to economic changes than equities, and it’s sniffing out the pivot (helped by cooling inflation registered in this week’s ISM services).

With so much doom and gloom, you’d think we’d be selling equities. We’re not. We need to see earnings and technicals change course to confirm our thesis, and that simply isn’t happening yet. We’re not calling for a recession, but having a 10-20% allocation to bonds (via TLT, for example) makes sense here. We will be watching labor statistics in the coming months for evidence.

Manufacturing head-fake

Looks like a good print, but there’s a different story under the hood…

The rest of this article is for paid subscribers. Upgrade below to continue reading:

Manufacturing PMI is not as bullish as it seems

Tariff threats in full force

Technical analysis and our outlook

2 actionable trade ideas

Keep reading with a 7-day free trial

Subscribe to MKTCONTEXT to keep reading this post and get 7 days of free access to the full post archives.