🍔BUY Signal Triggered

We sold the peak and bought near the bottom of the August selloff.

Welcome back to MktContext where we explain what’s happening in the US economy, and use that to time the stock market.

This week we share all our BUY signals. While a lot of naysayers called for recession, we sold the peak and caught the near-bottom of the recent selloff. If you’ve been following our signals, in July we avoided a 7% drawdown in SPX compared to a simple buy-and-hold strategy. Our trades and portfolio are shared in the premium section.

So what are you waiting for? For the small price of US$39, you could have saved THOUSANDS of dollars (if not tens of thousands) in just ONE month from the recent selloff. And we still have four months left in the year.

And if you aren’t a subscriber yet, do so now to get our FREE weekly posts.

Today’s topics: Macro economy still good, volatility receding, the BIG RISK next week, our trades last week, signals we used to time the market bottom, technical predictions for this year, and our current portfolio.

Macro economy review

We’ve been saying for MONTHS that the economy is strong (see here, here, here). “Ignore the bears, ignore the recession calls”… we sound like a broken record. When the disastrous jobs data came out two weeks ago, we knew it was an anomaly. This has kept us on the right trade all year long.

We got more jobs data this week. And it’s unequivocally good. Unemployment claims (tracks the number of people filing for unemployment benefits) was low. Retail sales (measures the total amount of sales made by stores, and speaks to consumer spending patterns) was positive. Remember, our thesis is that the consumer is more resilient than people think, which supports stock prices. If everyone is still out there spending, how bad can unemployment be?

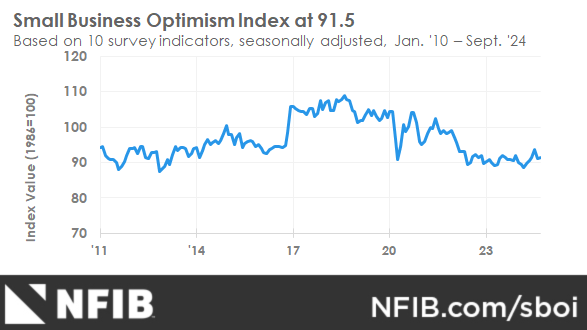

Small Business Optimism was the best it’s been in months. Small businesses hire a lot of workers and are an early indicator of economic growth. This survey told us they are hiring more, spending on equipment, increasing inventories, expanding their businesses, and overall expecting a better economy.

Inflation fell this week. We’ve been calling for falling inflation, giving the green light for the Fed to start cutting. One thing to note is that trade service inflation is coming down, and while that’s good for inflation, it’s not good for S&P500 profit margins. Any sign of margin compression will hit corporate earnings and derail the bull thesis.

All that said, it’s clear that jobs and the economy are slowing. That is, a normalization to trend, not outright deterioration. GDP is still near 3% and unemployment is stable. The rise in unemployment rate isn’t driven by falling labor demand (layoffs) but rather an increase in labor supply (immigration and labor force participation). That means it shouldn’t trigger job losses nor a drop in incomes; good news for the economy.

If you’re enjoying this post so far, like and share with a trader you know!

Volatility review

VIX subsided. I have already written a lot about VIX (check out my explainer on volatility!) so let’s introduce VIX term structure. This is a measure of present volatility VS future volatility. Since the present is more certain than the future, present volatility is almost always lower than future volatility. When the market expects an imminent crash, present volatility trades much higher than future volatility, and the structure is said to invert. After being inverted all of last week, the structure has un-inverted, telling us the market has calmed down:

The reason it didn’t turn into a full-blown crisis is because businesses are doing well and debt levels are low. In a crisis, falling asset prices impacts loan values which creates problems for banks. You will know credit is igniting because junk bonds and bond volatility start to blow up (shoutout to Alexander Campbell for explaining this!). This time, there was no contagion, no dry tinder to catch the spark. The credit markets were quite tame:

As an aside, this is why it’s important to marry macro economic analysis with technicals. A lot of people were just looking at the price charts and expecting a full-blown meltdown. But that’s a misreading of the context, and would have led to an incorrect bearish thesis.

Interest rates

With the growth scare still fresh in everyone’s minds, the market is now pricing in 4 or 5 rate cuts by the end of the year. This is a mistake. The Fed is unlikely to cut fast because of the aforementioned resilience in jobs. It’s incredible to me that intelligent people were calling for an emergency cut last week when the data clearly didn’t support it.

In fact, the market is implying we will see the third-fastest cutting cycle in 50 years. The only cycles when the Fed cut more aggressively were Covid and the Dot-Com crash. Does it feel like we’re in Covid or Dot-Com right now? NO.

There is simply no economic data warranting big cuts. Several Fed members publicly pushed back against big cuts. The Wall St. Journal’s Nick Timiraos (a.k.a. “Fed whisperer”, who has Powell on speed dial) said we need to see a weakening of the data to get a 50bp cut in Sept.

What does this all mean? Powell next speaks at Jackson Hole on Aug 23 and he too is likely to push back against big cuts. This “hawkish surprise” will hurt the bond market and possibly the stock market along with it. Expect volatility this week.

The rest of this article is for paid subscribers. Upgrade now to continue reading the rest:

Our big trade this week

6 signals we used to time the market bottom

Technical prediction for rest of the year

Our current portfolio

Claim your free trial by clicking the button below (or reply to this email and we’ll send you a trial directly).

Keep reading with a 7-day free trial

Subscribe to MKTCONTEXT to keep reading this post and get 7 days of free access to the full post archives.